Introduction

In an era where sustainability is no longer a choice but a necessity, the European Union (EU) has taken a significant step forward with the introduction of the Corporate Sustainability Reporting Directive (CSRD). The CSRD is a transformative piece of legislation that aims to improve the quality and scope of non-financial information disclosed by companies. It is a response to the growing demand from investors, regulators, and the public for more reliable and comparable sustainability information. The directive is part of a broader EU strategy to integrate sustainability considerations into its financial policy framework and corporate governance.

Sustainability reporting in the EU has been a journey of continuous improvement and expansion. Over the years, the EU has introduced several initiatives to promote transparency and accountability in corporate sustainability practices. The Non-Financial Reporting Directive (NFRD), introduced in 2014, was one such significant step. It required large public-interest entities, including listed companies, banks, and insurance companies, to disclose non-financial and diversity information.

The NFRD aimed to increase transparency and encourage companies to be more socially responsible. It required companies to report on environmental matters, social and employee-related aspects, respect for human rights, anti-corruption and bribery issues, and diversity in their board of directors. However, while the NFRD was a step in the right direction, it had its limitations.

One of the main criticisms of the NFRD was its limited scope. It only applied to large public-interest entities with more than 500 employees, leaving out a significant number of companies. Additionally, the directive was criticized for its lack of specificity. It did not provide detailed guidelines on what information companies should disclose, leading to inconsistencies in reporting practices.

Another limitation was the lack of mandatory assurance for non-financial information. Unlike financial information, which is subject to audit, non-financial information under the NFRD did not require independent verification. This raised concerns about the reliability and comparability of the reported information.

These limitations underscored the need for a more comprehensive and robust framework for sustainability reporting in the EU, leading to the introduction of the CSRD.

Key Features of the CSRD

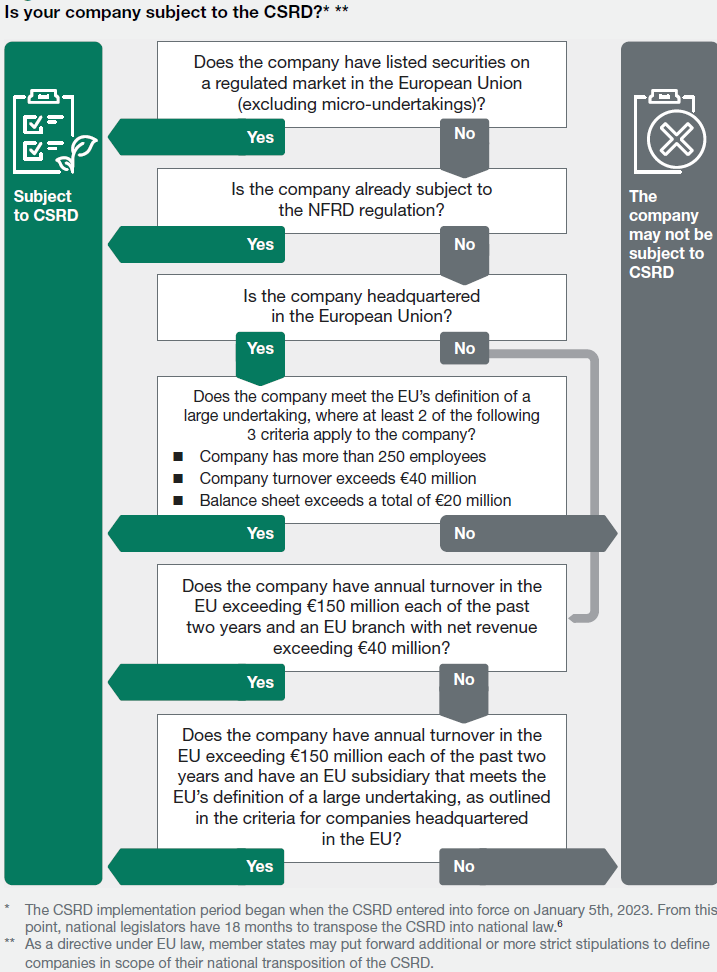

One of the key objectives of the CSRD is to expand the scope of companies required to disclose sustainability information. Unlike the NFRD, which only applied to large entities with more than 500 employees, the CSRD applies to all large companies and all companies listed on regulated markets (except for listed micro-enterprises). This means that an estimated 50,000 companies in the EU will be required to comply with the CSRD, compared to around 11,000 under the NFRD. The expanded scope of CSRD also applies to non-EU companies who have significant operations or presence in the EU. This expansion of scope is a significant step towards greater transparency and accountability in corporate sustainability practices.

The Corporate Sustainability Reporting Directive (CSRD) introduces several key features that set it apart from its predecessor, the Non-Financial Reporting Directive (NFRD).

Double Materiality

The double materiality principle is a central tenet of the CSRD. It requires companies to disclose information on both how their activities influence the environment and society, and how sustainability issues could impact their operations, financial performance and future prospects. This dual perspective makes sustainability reporting more comprehensive and relevant. It reflects an understanding that sustainability risks and opportunities can have significant implications for a company's performance. This principle also acknowledges that businesses have a responsibility not only to their shareholders, but also to the wider society and environment.

Mandatory Assurance of Sustainability Information

One of the most significant features of the CSRD is the mandatory assurance of sustainability information. Unlike the NFRD, which did not require independent verification of non-financial information, the CSRD requires companies to have their sustainability information assured by an external auditor. This is a crucial step towards improving the reliability and credibility of sustainability reporting.

Introduction of EU Sustainability Reporting Standards

The CSRD also introduces EU sustainability reporting standards (ESRS). These standards will provide detailed guidelines on what sustainability information companies should disclose and how they should disclose it. The aim is to ensure consistency and comparability in sustainability reporting across the EU. The development of these standards is overseen by the European Financial Reporting Advisory Group (EFRAG), which will work closely with stakeholders to ensure that the standards meet their needs.

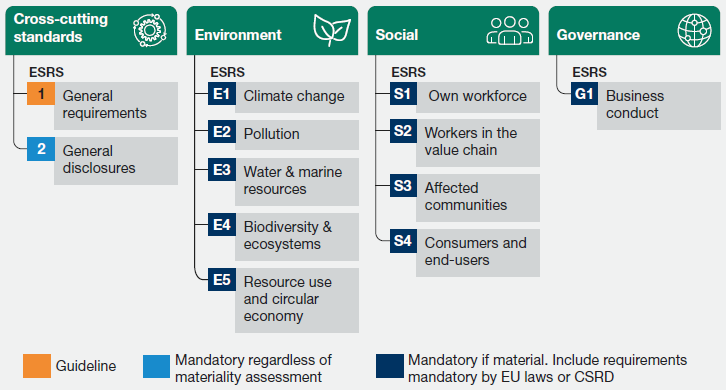

Pillars of the ESRS

Digital Format Requirement for Sustainability Reports

Another key feature of the CSRD is the digital format requirement for sustainability reports. Companies will be required to publish their sustainability information in a digital format that is machine-readable. This will make it easier for stakeholders to access and analyze the information, facilitating better decision-making. It will also enable the EU to create a central database of sustainability information, providing a valuable resource for investors, regulators, and the public.

Implications for Companies

The CSRD will require companies to adapt their reporting practices. They will need to familiarize themselves with the new EU sustainability reporting standards and ensure that their reporting processes are robust enough to meet the new requirements. They will also need to establish relationships with external auditors who can assure their sustainability information.

Another challenge is the need for companies to engage with a wide range of stakeholders, from investors and employees to regulators and the wider community. This can require a significant effort, but it is crucial for the credibility and effectiveness of sustainability reporting.

While the CSRD presents challenges, it also offers opportunities. By improving the quality and comparability of sustainability information, the CSRD can help companies gain the trust of investors, regulators, and the public. It can also encourage companies to take a more strategic approach to sustainability, integrating it into their core business operations and decision-making processes.

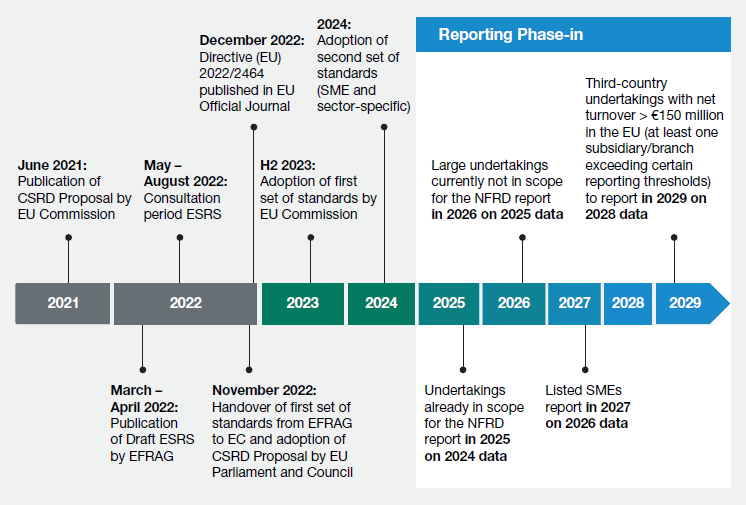

CSRD Regulatory Timeline

Conclusion

The CSRD is expected to have a profound impact on sustainability reporting in the EU. By expanding the scope of companies required to disclose sustainability information, introducing EU sustainability reporting standards, and requiring mandatory assurance of sustainability information, the CSRD will raise the bar for sustainability reporting.

In conclusion, the CSRD is a significant step forward in the EU's journey towards a sustainable economy. It presents challenges, but also opportunities for companies and stakeholders to contribute to a more sustainable future. As we navigate this new era of sustainability reporting, the key will be to embrace the spirit of the CSRD - not just its letter - and to use it as a tool for positive change.

At Keslio, we are deeply passionate about sustainability, equipping us with the expertise and extensive network needed to guide clients through their sustainability journey effectively and efficiently. Our expertise is particularly valuable for companies looking to embed sustainability practices into their businesses and investors looking to integrate ESG and impact into investment portfolios. To learn more about how Keslio can assist your organization on its sustainability journey, please don't hesitate to get in touch with us.